If there is a matrix, X,

If there is a matrix, X,

then the linear model can be written as

then the linear model can be written as

These notes are heavily based on Chapter 15 of Modeling Financial Time Series with S-Plus by Zivot and Wang, Second Edition, Springer, 2006. In places I have taken the liberty of copying complete sentences (or parts of sentences). Other material has been cribbed from Prof. Zivot's lecture notes for his Factor Models for Asset Returns lecture.

The S+ code in Zivot and Wang can be used almost without change in R. A few of the necessary changes have been taken from the code that Guy Yollen used in Financial Data Modeling and Analysis with R (AMATH 542), which is part of the University of Washington Computational Finance Master's program.

These notes are not intended to be an original work. They are not a paper or an article. So I hope that Prof. Zivot and Wang will not object to my borrowing their material. Any errors, however, are mine.

Factor models are linear models:

![]() where

where

![]() are

the predictor variables and

are

the predictor variables and

![]() is the response variable. Linear regression is used to estimate the

is the response variable. Linear regression is used to estimate the

![]() values.

The vectors

values.

The vectors

![]() are

If there is a matrix, X,

then the linear model can be written as

are

If there is a matrix, X,

then the linear model can be written as

![]() ,

where the

,

where the

![]() values are estimated via least squares. The least squares equation

to estimate

values are estimated via least squares. The least squares equation

to estimate

![]() is

is

![]() .

.

BARRA style single factor model:

![]()

The

![]() values

are known and are invariant (at least over the time period t =

1...T). The factor value,

values

are known and are invariant (at least over the time period t =

1...T). The factor value,

![]() is estimated from the data. An example of such a

is estimated from the data. An example of such a

![]() value would be industry sector and industry membership for a stock.

Here each stock, i = 1...N, has its asset specific value of

value would be industry sector and industry membership for a stock.

Here each stock, i = 1...N, has its asset specific value of

![]() .

.

The expression for a mutli-factor model is:

![]() where

where

![]() is the return (real or in excess of the risk free rate) on asset i (i

= 1..N) in time period t (t = 1..T). This is a linear

factor model, where

is the return (real or in excess of the risk free rate) on asset i (i

= 1..N) in time period t (t = 1..T). This is a linear

factor model, where

![]() is

the intercept,

is

the intercept,

![]() is

the

is

the

![]() common factor (k = 1..K),

common factor (k = 1..K),

![]() is

the factor loading or factor beta for asset i on the

is

the factor loading or factor beta for asset i on the

![]() factor, and

factor, and

![]() is the asset specific factor.

is the asset specific factor.

The return on asset 1, at time t1 is

A cross sectional view of the factor model is shown in the equation below. Here the cross section is across a single unit of time, t1. Here the cross sectional return for all of the assets (I = 1..N) is calculated at time t1.

![]()

This can be rewritten incorporating the intercept term (the

![]() values)

into the beta matrix:

values)

into the beta matrix:

![]()

In the fundamental factor model, the beta values (B) are

known and the factor values (![]() )

are unknown.

)

are unknown.

The ordinary least squares equation for

![]() (for

multiple linear regression) is:

(for

multiple linear regression) is:

![]() where the B values are

invariant (for example, industry membership) and the

where the B values are

invariant (for example, industry membership) and the

![]() values

are the returns. To calculate the cross sectional regression

we calculate the factor realizations

values

are the returns. To calculate the cross sectional regression

we calculate the factor realizations

![]()

In portfolio construction factor models are used to estimate the

covariance matrix,

![]() ,

that is used to estimate the optimal portfolio (either the

mean-variance or CVaR optimal portfolio).

,

that is used to estimate the optimal portfolio (either the

mean-variance or CVaR optimal portfolio).

The beta values,

![]() (for asset i and industry k) are 1 if asset i is

in industry k, and zero otherwise.

(for asset i and industry k) are 1 if asset i is

in industry k, and zero otherwise.

The factor values,

![]() (for

industry k at time t, t = 1...T) are equal to the

weighted excess return for the firms in the portfolio that are in

industry k.

(for

industry k at time t, t = 1...T) are equal to the

weighted excess return for the firms in the portfolio that are in

industry k.

To estimate the weighted least squares we first need to find the error variance. This is found via ordinary least squares of the result of the cross sectional regression, at time t.

The BARRA style industry factors

![]() are

stored in the matrix B (here

we can assume that the matrix has the column and row names shown

below):

are

stored in the matrix B (here

we can assume that the matrix has the column and row names shown

below):

|

|

TECH |

OIL |

OTHER |

|

CITCRP |

0 |

0 |

1 |

|

CONED |

0 |

0 |

1 |

|

CONTIL |

0 |

1 |

0 |

|

DATGEN |

0 |

0 |

1 |

|

DEC |

1 |

0 |

0 |

|

DELTA |

0 |

1 |

0 |

|

GENMIL |

0 |

0 |

1 |

|

GERBER |

0 |

0 |

1 |

|

IBM |

1 |

0 |

0 |

|

MOBIL |

0 |

1 |

0 |

|

PANAM |

0 |

1 |

0 |

|

PSNH |

0 |

0 |

1 |

|

TANDY |

1 |

0 |

0 |

|

TEXACO |

0 |

1 |

0 |

|

WEYER |

0 |

0 |

1 |

There is also a matrix of returns

![]() for fifteen stocks listed above. To estimate

for fifteen stocks listed above. To estimate

![]() :

:

![]()

F.hat = solve(t(B) %*% B) %*% t(B) %*% t(returns)

Calculate the residual variances and

build the

![]() matrix. The

matrix. The

![]() matrix is a diagonal matrix containing the

matrix is a diagonal matrix containing the

![]() values.

values.

In least the least squares equation

above, the residual variance is

![]() .

Here the residual variance is

.

Here the residual variance is

![]()

E.hat = t(returns) - B %*% F.hat

Calculate the variances across the rows

diagD.hat = apply(E.hat, 1, var)

Dinv.hat = diag( diagD.hat^(-1))

Note that the inverse of the matrix D

![]() is the same as the inverse of the values on the diagonal:

is the same as the inverse of the values on the diagonal:

identical(solve(diag(diagD.hat)), diag(diagD.hat^(-1))) is TRUE

![]()

# multivariate FGLS regression to estimate K x T matrix of factor returns

H = solve(t(B) %*% Dinv.hat %*% B) %*% t(B) %*% Dinv.hat

# create factor mimicking portfolios

F.hat = H %*% t(returns)

colnames(H) = colnames(returns)

F.hat = t(F.hat)

The rows of the H matrix contain the weights for the factor mimicking portfolio:

|

|

TECH |

OIL |

OTHER |

|

CITCRP |

0 |

0 |

0.1992 |

|

CONED |

0 |

0 |

0.2202 |

|

CONTIL |

0 |

0.0961 |

0 |

|

DATGEN |

0.2197 |

0 |

0 |

|

DEC |

0.3188 |

0 |

0 |

|

DELTA |

0 |

0.2233 |

0 |

|

GENMIL |

0 |

0 |

0.2297 |

|

GERBER |

0 |

0 |

0.127 |

|

IBM |

0.281 |

0 |

0 |

|

MOBIL |

0 |

0.2865 |

0 |

|

PANAM |

0 |

0.1186 |

0 |

|

PSNH |

0 |

0 |

0.0668 |

|

TANDY |

0.1806 |

0 |

0 |

|

TEXACO |

0 |

0.2756 |

0 |

|

WEYER |

0 |

0 |

0.1571 |

Estimation of Industry Factor Model Asset Return Covariance Matrix. The covariance matrix of the N assets is then estimated by:

cov.ind = B %*% var(F.hat) %*% t(B) + diag(diagD.hat)

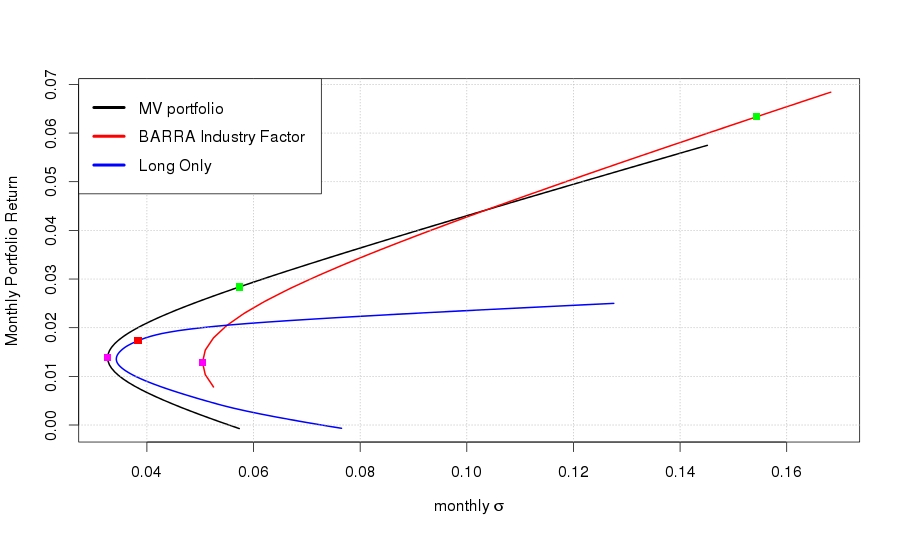

The plot below shows efficient frontiers for a mean-variance optimized long/short portfolio, the BARRA industry factor model, developed above and a mean-variance long only portfolio.

A listing of the complete R code can be found here.

The R code and the model data can be downloaded here:

The Fama-French approach for estimating

![]() for

a given characteristic (for example market capitalization size) they

use a two step process:

for

a given characteristic (for example market capitalization size) they

use a two step process:

Sort the cross section of assets based on the values of the asset specific characteristics.

Form a hedged portfolio that is long in the top quintile (e.g., top 20%) for the characteristic and short in the bottom quintile of the sorted assets. This portfolio is a dollar neutral portfolio (e.g., as much on the long side as the short side).

The return on the hedged portfolio at time t is the observed

factor realization for the asset specific characteristic

![]() .

The process is repeated for each factor, over the time period t =

1..T.

.

The process is repeated for each factor, over the time period t =

1..T.

This gives us a set of cross sectional values for each factor i, i

= 1...N. The factor

![]() values

are estimated using N time series regressions.

values

are estimated using N time series regressions.

The factor model can also be expressed as a time series model,

where the return on asset

![]() is

calculated across the time period t = 1...T.

is

calculated across the time period t = 1...T.

![]()

For BARRA style fundamental factor models, the

![]() values

are constant and the factor realizations at time t,

values

are constant and the factor realizations at time t,

![]() are

estimated from the data.

are

estimated from the data.

This can be written as the ordinary least squares equation

![]()

back to Topics in Quantitative Finance